Understanding Chargebacks

What Are Chargebacks?

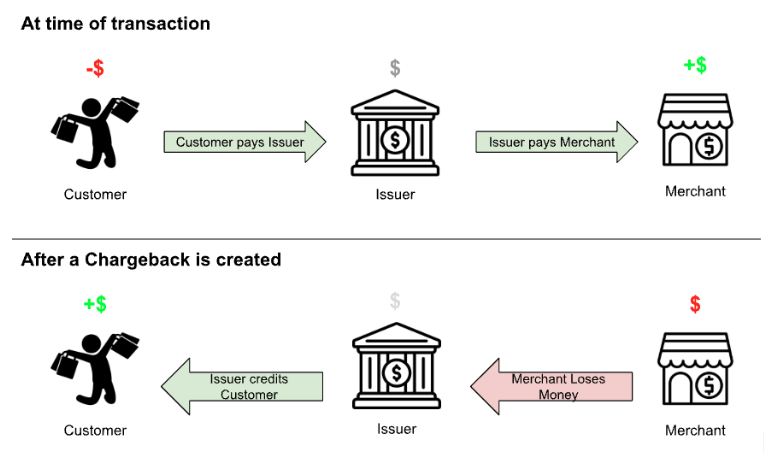

A chargeback is a transaction reversal initiated by a cardholder after a payment has been processed. It occurs when a customer disputes a charge with their bank instead of contacting the merchant. The bank evaluates the claim and, if approved, forcibly reverses the transaction—removing funds from the merchant’s account and returning them to the cardholder.

Unlike refunds, chargebacks bypass the merchant and are typically more costly, involving fees, penalties, and possible increases in dispute ratios.

Purpose of Chargebacks

Chargebacks serve two primary purposes:

- Customer Protection: Enables consumers to recover funds in cases of fraud or merchant misconduct.

- Merchant Accountability: Encourages transparent practices and discourages negligence.

Types of Chargebacks

Chargebacks generally fall into two broad categories based on the reason code:

Fraud-Related Chargebacks

These occur when the cardholder claims they did not authorize the transaction. This includes cases of:

- Stolen credit card information

- Unauthorized use

- Account takeover

Service-Related Chargebacks

These stem from merchant errors or issues with the transaction, such as:

- Non-delivery of goods or services

- Incorrect charges

- Miscommunication or dissatisfaction

Chargeback Reason Codes

Each card network assigns a reason code to explain why the chargeback was initiated. These codes determine:

- The dispute reason

- Required evidence

- Response deadlines

- Prevention guidelines

Visa, Mastercard, Amex, and other networks maintain their own code sets, and accurate interpretation is critical for effective resolution.

Chargebacks vs. Refunds

While both chargebacks and refunds result in funds being returned to the customer, the key difference lies in how they are initiated and processed:

| Refund | Chargeback | |

|---|---|---|

| Initiated by | Merchant | Customer via issuing bank |

| Process flow | Voluntary, via merchant system | Involuntary, via issuing bank |

| Revenue Loss | Predictable and planned | Unexpected; merchant often unaware |

| Merchandise | Can be returned and resold | Usually not returned, as merchant is left out of the conversation |

| Cost implications | Typically no fees | Includes penalties, fees, and affects dispute ratios |

How Funds Are Reversed

Lifecycle of a Chargeback

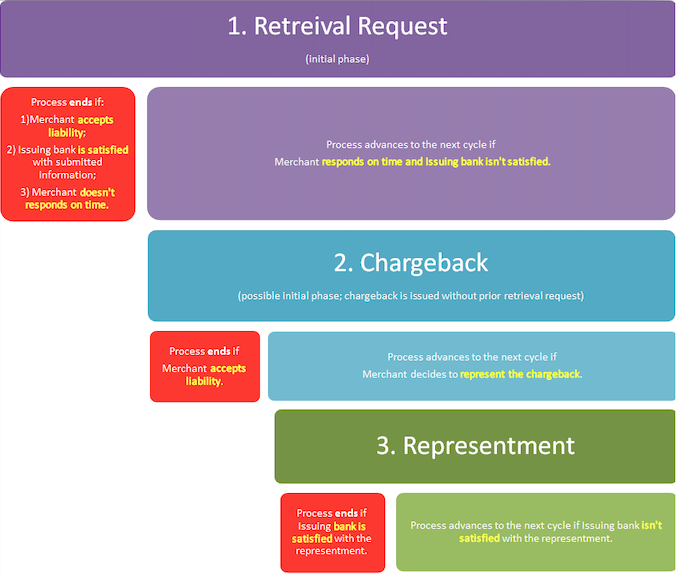

- Retrieval Request -- (only for Discover, Amex) The issuer requests information before creating a formal chargeback. This is also known as request for information (RFI)

- Chargeback – The merchant is notified, and funds are withdrawn. The merchant can accept or fight the chargeback.

- Representment – If the merchant disputes the chargeback, they submit evidence to prove legitimacy in the form of a PDF (also known as the dispute letter). The bank then evaluates the case, compares it to the network rule books, and makes a decision.

Benefits of Adding Evidence

When submitting a chargeback representment, providing evidence strengthens the merchant’s position in a dispute:

- Fraud Chargebacks: Demonstrate that the cardholder authorized the transaction.

- Service Chargebacks: Prove merchant complied with terms of service or delivery policies.

More compelling evidence increases the likelihood of a win.

Updated about 1 month ago